India Mobile Handsets market ends on a lower note in 2015 as transition gathers momentum

Share This Post

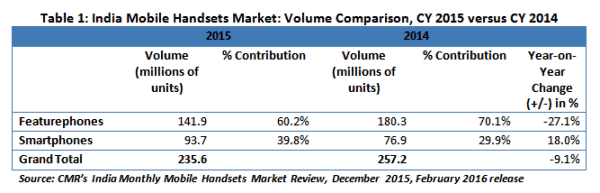

Market clocks 235.6mn unit shipments, down 9.1% from CY 2014

- 40% of the handsets sold were Smartphones

- Samsung, Micromax and Intex lead, in that order, for overall as well as Smartphones segment; Lenovo makes significant gains

- 2G Smartphones now a ‘dead’ segment with just 9% contribution to overall smartphone shipments in 2015; 4G growing fast

- Market expected to settle at 250 mn units in 2016, including 130 mn Smartphones

New Delhi/Gurgaon: Tuesday, February 2, 2016 – Announcing the annual report card for the India Mobile Handsets market for CY 2015 today, a CMR report said that the country sold 235.6 million units in the year as compared to 257.2 million units in 2014, down 9.1% year-on-year.

Smartphones, which constituted 39.8% of the total sales, grew at 18% while Featurephones registered a sharp decline of 27.1% in annual shipments.

Commenting on the highlights of the report, Faisal Kawoosa, Lead Telecoms Analyst, CMR said, “We are witnessing a transition period for the industry. Transition from mass to niche, featurephones to Smartphones, 2G and 3G to 4G, ‘offline only’ to hybrid, that is, a combination of offline and online, and ‘imports only’ to domestic manufacturing with imports. This transition phase is bound to result in a contraction of the market in volume terms, which is what we saw towards the end of calendar year 2015, in particular.”

“Once this transition is over and vendors adopt the right mix of sourcing and marketing, and develop competencies to address the emerging/niche segments rather than the mass market, we should see the market rebound back,” Faisal added.

Year 2015 saw the entry of twenty (20) Smartphone brands into the India market, taking the total options a consumer could choose from to 161. Overall, there were 431 brands selling mobile phones in the country.

Commenting on this trend, Karn Chauhan, Analyst for the India Mobile Device market at CMR said, “This year the ‘Top 10’ Smartphone brands contributed to 82.9% of shipments, compared to 85.1% in 2014. We expect the market to fragment further and while this is a healthy sign, ending the dominance of a few players, what is worrying is the ability of new entrants to sustain their performance.”

“We have observed that most brands lose vigour after a quarter or two of their entering the market. Unfortunately, they are not able to keep up the momentum in terms of shipment volumes that they initially disrupt the market with. This leads to fluctuations in overall shipments and market shares – one of the results and inconsistencies that we saw in 2015,” Karn concluded.

Share This Post

CyberMedia Research conducts the Budget Smartphones Channel Audit to capture the perspectives, preferences, challenges and dislikes of retailers around ‘value for money’ (INR <10,000) smartphone brands, capturing a compelling picture of smartphone brands in the market.

CMR offers industry intelligence, consulting and marketing services, including but not limited to market tracking, market sizing, stakeholder satisfaction, analytics and opportunity assessment studies.

Its bouquet of consulting services includes incubation advisory, go-to-market services, market mapping and scenario assessment services. CMR is servicing domestic as well as international clientele in India and few global destinations. The clientele serviced represents SMBs, Large Enterprises, Associations and Government. CMR’s core value proposition encompasses a rich portfolio of syndicated reports and custom research capabilities across multiple industries, markets and geographies. For details on the survey findings, ping Satya Sundar Mohanty at smohanty@cmrindia.com, or call +919821690824.

A part of CyberMedia, South Asia’s largest specialty media and media services group, CyberMedia Research (CMR) has been a front-runner in market research, consulting and advisory services since 1986. CMR is an institutional member of Market Research Society of India (MRSI).

More To Explore

No posts found!