India’s smartphone market is undergoing a structural shift in storage preferences, driven by rising premiumization and the rapid expansion of AI-led smartphone usage. Between Q1 2023 and Q1 2026, Indian consumers steadily migrated toward higher-storage smartphone variants as smartphones evolved into primary devices for entertainment, gaming, productivity, content creation, and increasingly, AI-powered experiences.

What was once considered a premium specification has now become mainstream. Storage capacity is no longer a secondary hardware parameter — it is emerging as a key purchase driver across price segments, influencing both consumer behaviour and OEM portfolio strategy.

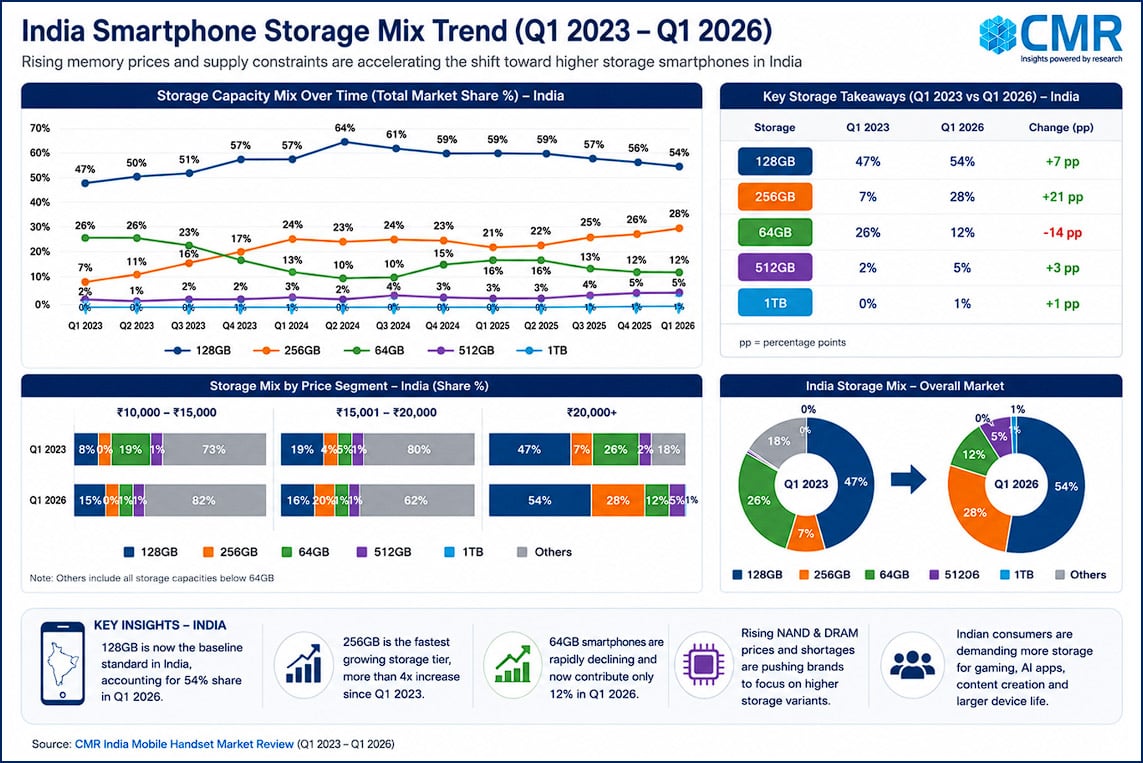

The strongest evidence of this transition has been the rise of 128GB smartphones as India’s default storage standard. The segment expanded from 47% market share in Q1 2023 to a peak of 64% in Q2 2024 before stabilizing at 54% by Q1 2026. Much of this momentum came from the ₹10,000–₹20,000 segment, where consumers increasingly prioritized long-term usability and smoother everyday performance over entry-level affordability.

This shift reflects changing smartphone usage patterns among Indian consumers. Users today store significantly larger volumes of data directly on-device, including high-resolution photos, OTT downloads, gaming assets, creator tools, AI applications, and 5G video content. As application sizes expanded and digital consumption intensified, 64GB devices increasingly became inadequate for mainstream usage.

Smartphone brands responded by aggressively pushing 128GB variants across broader price tiers to improve user experience while reducing storage-related performance bottlenecks.

At the same time, India witnessed a sharp acceleration in 256GB smartphone adoption, particularly in the premium and upper mid-range segments. The 256GB category grew from just 7% market share in Q1 2023 to 28% by Q1 2026, underscoring how premiumization is reshaping consumer expectations. Devices priced above ₹20,000 increasingly shifted toward 256GB as a standard configuration rather than an optional upgrade.

The rise of AI smartphones further accelerated this transition. AI-powered photography, generative AI applications, advanced video editing, and on-device AI assistants require significantly higher local storage capacity. Consumers purchasing premium smartphones are increasingly looking for devices capable of handling heavier multitasking and richer AI-led experiences over longer ownership cycles.

This marks an important shift in India’s smartphone market. Premiumization is no longer defined only by processors, cameras, or industrial design. Storage capacity itself has emerged as a visible marker of device quality, longevity, and overall value.

As higher-storage variants gained momentum, lower-storage devices rapidly lost relevance. The 64GB segment declined from 26% market share in Q1 2023 to just 12% by Q1 2026, while 32GB smartphones virtually disappeared after 2024. Larger Android operating systems, rising gaming adoption, AI-enabled applications, expanding 5G video usage, and creator-led smartphone consumption collectively accelerated the decline of lower-storage devices.

Even in the sub-₹10,000 segment, smartphone brands increasingly shifted toward offering 128GB storage to improve competitiveness and strengthen value perception.

The transition also reshaped OEM portfolio strategies. Earlier, brands relied on wider SKU portfolios and aggressive entry-level pricing to maximize shipment volumes. However, from late 2024 onward, smartphone brands increasingly simplified portfolios, reduced lower-storage variants, and prioritized higher-storage configurations. Storage upselling emerged as an important lever for improving ASPs and strengthening profitability, while 128GB and 256GB configurations became the market’s strategic sweet spots.

India’s smartphone storage transition now reflects a broader evolution in the market itself — toward longer ownership cycles, AI-ready hardware, and more value-driven premiumization.

The rapid disappearance of 32GB smartphones highlights how sharply baseline consumer expectations have evolved. Entry-level smartphones are no longer expected to support only communication and light app usage. They are increasingly being used for streaming, gaming, creator tools, AI-assisted applications, and heavier multitasking, fundamentally raising the minimum viable storage threshold across the market.

At the same time, leading smartphone brands are repositioning storage configurations to strengthen both consumer value perception and profitability.

Over the next two to three years, the gap between mainstream and premium storage standards is expected to narrow further. As AI-driven experiences become more deeply integrated into everyday smartphone usage, storage capacity will increasingly influence device longevity, resale value, and overall consumer satisfaction. In this environment, brands that align storage strategy with evolving usage behaviour — rather than competing purely on pricing — are likely to be better positioned to capture the next phase of smartphone value growth in India.

At the same time, leading smartphone brands are strategically repositioning storage configurations to strengthen both consumer value perception and profitability. Samsung and Apple continue to anchor premium storage expectations at the higher end of the market, while brands such as Xiaomi, realme, and OnePlus are increasingly pushing higher-storage variants deeper into mid-range price tiers to accelerate premiumization at scale.

Over the next two to three years, India’s smartphone market is likely to witness a faster convergence between mainstream and premium storage standards. As replacement cycles lengthen and AI-driven experiences become more deeply integrated into everyday smartphone usage, storage capacity will increasingly influence device relevance, resale value, and long-term consumer satisfaction. In that environment, brands that align storage strategy with evolving usage behaviour — rather than relying solely on pricing-led competition — are likely to be better positioned to capture the next phase of smartphone value growth in India.