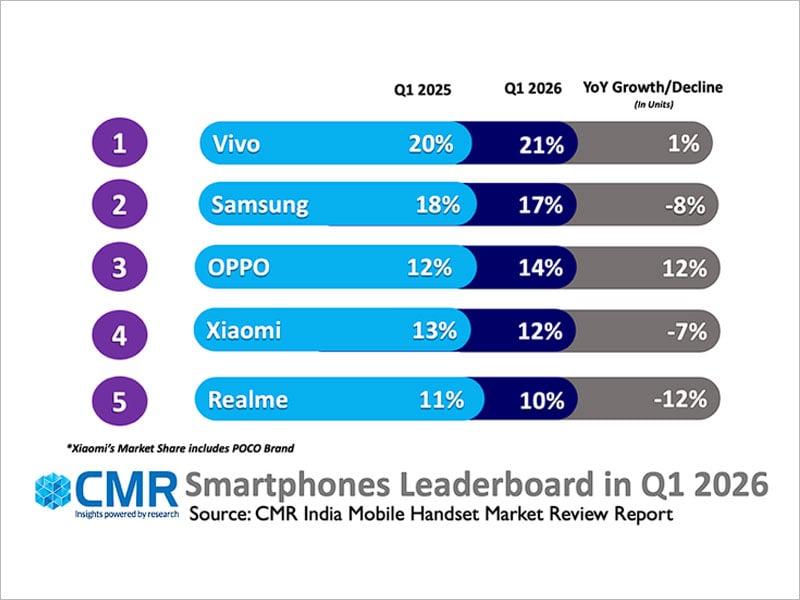

- Vivo led the India smartphone market in Q1 2026 with 21% share, followed by Samsung (17%) and OPPO (14%).

- Apple drove premium segment momentum, posting a6% YoY growth and 9% market share.

- CMR warns of a double-digit decline for the full year.

New Delhi/Gurugram, 04 May 2026: India’s smartphone market has hit weakest quarterly performance in recent years, with shipments declining 2% year-on-year in Q1 2026, according to the CMR India Mobile Handset Market Review Report released today by CyberMedia Research (CMR). The slowdown was driven by a sharp rise in DRAM and NAND flash prices, which pushed up device costs and forced brands to increase pricing—leading price-sensitive consumers to defer upgrades. The impact was sharply uneven across segments: while the premium segment grew 25%, the affordable segment declined 46% and the value-for-money segment fell 12%.

Vivo led India’s smartphone market with a 21% market share, followed by Samsung (17%), OPPO (14%), and Xiaomi (12%). Vivo also topped the 5G smartphone segment with a 23% share, closely followed by Samsung at 16%.

Commenting on the market dynamics, Menka Kumari, Senior Analyst – Industry Intelligence Group (IIG), CyberMedia Research (CMR) said, “India’s smartphone market entered 2026 under clear cost pressure, largely driven by ongoing memory supply constraints. A sharp rise in DRAM and NAND prices has increased device costs, forcing brands to recalibrate pricing across segments. This has resulted in slower upgrade cycles and softer momentum during the quarter. The impact is most pronounced in the value-for-money segment, where price sensitivity remains high. At the same time, the market is undergoing a structural shift. Consumers are becoming more deliberate in their purchase decisions, prioritising tangible value over frequent upgrades.”

Feature Phone Segment

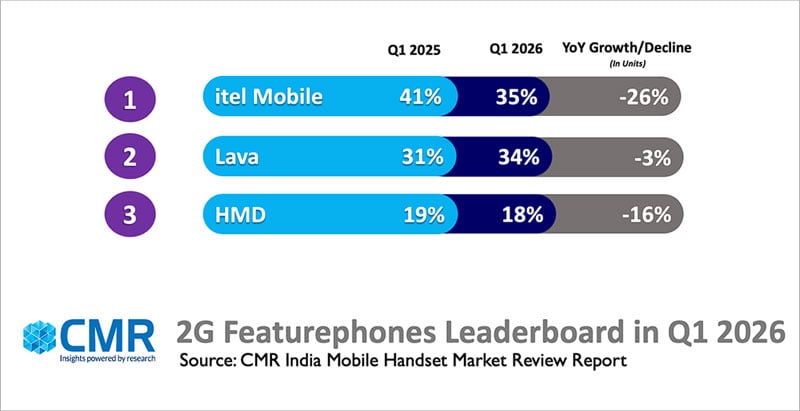

The feature phone segment deepened its structural decline in Q1 2026. The 2G segment fell 12% YoY, while 4G feature phones collapsed 41% YoY — underscoring accelerating consumer migration away from basic devices. Itel Mobile led the 2G segment with 35% share, followed by Lava (34%) and HMD (18%). Despite holding the top position, Itel saw a 26% YoY decline; Lava‘s modest 3% decline was a rare bright spot in an otherwise bruising quarter.

Q1 2026: Key Smartphone Market Highlights

Vivo captured the top spot with 21% market share. The Vivo Y31 5G, V60e, Y400, and Y31 Pro models alone drove 39% of its 5G shipments — a clear validation of its value-for-money smartphone playbook.

Samsung secured second place with 17% overall market share. Its portfolio spans price tiers effectively, with the Galaxy A17 and A07 driving the value-for-money segment (12% combined share), while the S26 Ultra anchors its ultra-premium positioning.

OPPO was the quarter’s standout performer at third place with 14% market share and shipments up 12% YoY — the strongest growth among top-five brands in a declining market — driven by a refreshed OPPO A6 Series portfolio that resonated across both value-for-money (₹7,000–₹25,000) and premium (>₹25,000) consumers.

Xiaomi held 12% market share (down 7% YoY). Its newly launched Redmi 15A helped arrest a sharper decline, sustaining volumes while supporting a smoother portfolio transition.

Apple reached 9% shipment share in Q1 2026. The iPhone 16 series contributed 53% of volumes, while the newly launched iPhone 17 series captured 28% share — a healthy upgrade cycle that validates the premium segment’s relative insulation from memory-driven pricing stress.

OnePlus recorded a 28% YoY shipment decline in Q1 2026. However, the brand portfolio refresh paints a more nuanced picture: the OnePlus 15 series (15 and 15R) contributed 48% of volumes, with early OnePlus 15R traction pointed to growing consumer appetite in the upper mid-premium segment. The OnePlus Nord lineup — led by Nord CE 5 and Nord 5 — continued to anchor volumes at 39% share.

Transsion shipments fell 30% YoY in Q1 2026, its entry-level concentration proving a structural liability as rising prices and channel inventory corrections hit that segment hardest.

MediaTek led India’s smartphone chipset market with 48% share. Qualcomm led the premium segment (>₹25,000) with 36% market share.

Future Outlook

CMR projects a 10–12% full-year decline for India’s smartphone market in CY2026, with the affordable and value-for-money segments likely to see continued volume pressure, margin compression, and cautious consumer demand.

“Near-term demand will remain uneven, with price-sensitive consumers in the affordable and value-for-money segments deferring upgrades amid sustained cost pressures. As OEMs intensify their premium focus, a clear gap is emerging—the ₹5,000–₹15,000 segment is being left underserved. For smartphone OEMs that can deliver differentiated value at accessible price points, this represents a significant and largely untapped opportunity,” added Amit Sharma, Senior Analyst – Industry Intelligence Group (IIG), CyberMedia Research (CMR).